A lot of employers hear about IRS code section 125 and assume it is something complicated that only large companies need to worry about. In reality, it is one of the most practical ways to make employee benefits work harder without pushing business costs higher.

At its core, section 125 of IRS code allows employees to pay for certain qualified benefits using pre-tax dollars. That means taxable wages go down, which lowers payroll taxes for both the employee and the employer. For businesses trying to control expenses while still offering meaningful support, that matters more than ever.

A properly structured Section 125 plan creates room for tax savings while giving employees access to benefits they actually use. It is not about adding another complicated layer to payroll. It is about using a part of the tax code that already exists and applying it correctly.

What a Section 125 Plan Actually Does

The easiest way to understand IRS 125 is to think of it as a legal framework that lets employees choose certain benefits before taxes are calculated.

Because those deductions happen before federal income tax, Social Security tax, and Medicare tax are applied, taxable payroll drops. That reduction creates direct savings for the employer.

This is why many businesses use an IRS Section 125 Cafeteria Plan to strengthen benefits without increasing payroll burden.

A typical setup may include:

- health-related supplemental benefits

- wellness support

- telemedicine access

- family coverage options

- life insurance components

- employee assistance resources

The reason it is called a cafeteria plan is simple. Employees are given access to qualified benefit options rather than a single fixed benefit.

Why Employers Pay Attention to Section 125 Savings

The financial side is what usually gets attention first.

When taxable wages are reduced under section 125, employers pay less in payroll taxes for every participating W2 employee. Over a full year, that can create meaningful savings without changing the salary structure.

For example, some employers use structured plans that generate annual savings while also funding benefits such as:

- 24/7 virtual care

- family medical support

- mental health counseling

- prescription coverage with no copays

- group term life insurance

That is why a tax-advantaged benefit plan often becomes more attractive than simply adding another expensive benefit line item.

The savings are predictable, but only when the plan is set up correctly and administered under current IRS rules.

Why Employees Usually Value It More Than Expected

Employees often do not care about tax language. They care about whether a benefit helps at home.

That is where flexible benefit plans become practical.

A strong Section 125 structure can support benefits that apply not only to the employee but also to a spouse and dependents. That family piece often changes how people view the plan because it reaches beyond the workplace.

For many workers, benefits become more valuable when they include:

- family telemedicine visits

- counseling support

- urgent care access

- prescription help at zero copay

- group term life insurance protection

The life insurance side especially stands out because employees often do not realize how expensive individual coverage can be until they price it on their own.

When that protection is included through employer sponsored benefits, it feels immediately useful.

Why Compliance Matters More Than Most Employers Think

A section 125 plan only works when documentation and administration follow IRS requirements.

This includes:

- written plan documents

- election procedures

- payroll coordination

- qualifying event handling

- proper benefit eligibility tracking

Without those pieces, tax advantages can become difficult to defend during review.

That is why IRS qualifying events rules matter so much.

Employees cannot simply change benefit elections whenever they want during the year unless a qualifying event happens.

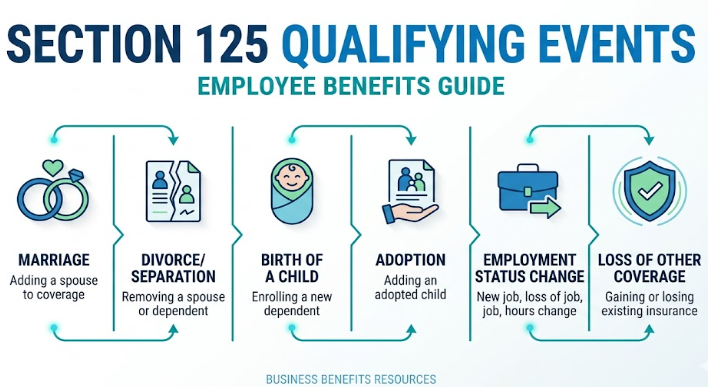

Common Section 125 Qualifying Events Employers Should Know

The IRS allows midyear benefit changes only under approved circumstances known as Section 125 qualifying events.

These usually include:

- marriage

- divorce

- birth of a child

- adoption

- death of a dependent

- loss of other coverage

- major employment status changes

These events exist because benefit elections are meant to stay stable unless life changes justify adjustment.

Employers who misunderstand this area often create avoidable compliance problems.

Why Modern Businesses Use Structured Plans Instead of Generic Benefits

Many companies already offer benefits, but not every benefit structure creates tax efficiency.

A properly managed Section 125 of IRS code strategy turns payroll tax savings into something employees can actually feel.

For example, some modern plan models include:

- employer tax savings per W2 employee

- reduced healthcare related spending

- zero copay prescription access

- spouse and dependent coverage

- group term life insurance value built into the plan

That is where businesses start seeing that tax savings and employee support do not have to compete with each other.

How Health Sphere Fits Into This

Health Sphere helps employers apply these rules through structured benefit plans that stay compliant while creating practical value for both sides.

Their approach focuses on making Section 125 simple enough to implement without forcing businesses to rebuild their current benefit setup.

Plans like Revive and Thrive are designed around that idea: tax savings first, but with benefits employees actually notice in daily life.

That can mean family access to care, counseling, life insurance, and prescription support, all built into a compliant framework.

Final Thought

A lot of employers ignore IRS code section 125 because it sounds technical. In practice, it is one of the few tax tools that can lower payroll costs while improving benefit value at the same time.

When handled correctly, it creates a cleaner way to support employees without adding unnecessary expense.

If your current benefits feel expensive but underused, Health Sphere can show you how a properly structured Section 125 strategy may create more value from the payroll dollars you already spend.

Want to See What Your Payroll Savings Could Look Like?

FAQs

How does an IRS Code Section 125 plan work?

A Section 125 plan works by taking eligible benefit costs out of payroll before taxes hit. That lowers taxable income right away. Employees usually notice it through better take-home value, while employers notice it through lower payroll tax costs. Same paycheck system, just used in a smarter way.

What are the benefits of IRS Code Section 125?

The biggest win is that both sides benefit at the same time. Employees get access to useful support without paying full after-tax dollars, and employers reduce payroll tax expense. When the plan is built well, it can also include real benefits families actually use, not just paperwork benefits.

Who is eligible for a Section 125 plan?

In most cases, W2 employees can join if their employer offers the plan and they meet the basic eligibility rules. Some businesses have a short waiting period before enrollment starts. The exact rules depend on how the employer sets up the plan documents.

What expenses are covered under IRS Code Section 125?

That depends on the plan, but most cover qualified health-related benefits like virtual care, prescription support, counseling, and certain insurance features. Some plans also extend those benefits.